Hargreaves Lansdown SIPP Review 2026

Index

Hargreaves Lansdown was founded in 1981 and has steadily grown into one of the UK's largest and most trusted investment platforms. Initially focusing on fund research, the company has expanded into providing a broad range of investment services including ISAs, SIPPs, and general investment accounts. Their reputation rests on delivering strong customer support, user-friendly tools, and a wide selection of investment choices. As of 2026, HL manages over £172 billion in client assets and serves more than half a million SIPP clients.

In this article, we will dive deeper into the Hargreaves Lansdown SIPP — exploring its features, fees, flexibility, and whether it might be the right pension solution for you.

What Is a Hargreaves Lansdown SIPP?

A Hargreaves Lansdown SIPP (Self-Invested Personal Pension) is a flexible pension product designed for individuals who want full control over their retirement savings. Unlike traditional pensions, a SIPP lets you choose where to invest your money from a wide selection of assets including stocks, funds, ETFs, and bonds.

This means you can tailor your pension to match your risk appetite, financial goals, and investment preferences. With a Hargreaves Lansdown SIPP, you benefit from tax advantages on contributions and growth, as well as a regulated framework ensuring your investments are protected.

Hargreaves Lansdown is one of the top platforms for SIPPs in the UK, managing over half a million pension clients. Their extensive research capabilities, combined with a strong digital platform, make them a popular choice for both novice and experienced investors looking to manage their pensions independently. In March 2026, HL implemented its first major fee overhaul in over 10 years — cutting its headline platform charge while restructuring some specific costs.

For more information on Hargreaves Lansdown and other alternatives to a SIPP, read our Hargreaves Lansdown review.

Main Features

Types of Investments Available

The Hargreaves Lansdown SIPP supports an extensive range of investments. You can choose from thousands of UK and international shares, investment trusts, unit trusts, ETFs, and government or corporate bonds. The platform also allows holding cash within the SIPP, and in response to the common question, does Hargreaves Lansdown pay interest on cash in SIPP? – yes, but the interest rates on cash balances within the SIPP tend to be modest compared to external savings accounts.

Flexibility & Withdrawal Options

HL offers flexible options for taking your pension benefits. From age 55 (increasing to 57 in 2028), you can withdraw lump sums or set up regular income payments. You're entitled to take 25% of your pension pot tax-free, with subsequent withdrawals taxed as income. This flexibility helps retirees tailor their income to their lifestyle and financial needs.

Tax Implications

Investments within a SIPP grow free of capital gains tax and income tax. Contributions attract tax relief based on your income tax bracket — between 20% and 45% — making SIPPs a highly tax-efficient vehicle for retirement saving. Withdrawals after age 55 are taxed as income, except for the tax-free lump sum, so planning your withdrawals is important to manage tax liabilities.

Fees and charges

When considering a Hargreaves Lansdown SIPP, understanding the associated costs is essential. In March 2026, HL overhauled its fee structure for the first time in over 10 years — cutting some charges while increasing others. The new fees took effect from 1 March 2026.

Here are the key changes under the new pricing plan:

- Annual platform fee reduced: from 0.45% to 0.35% on the first £250,000 (0.25% on the next £750,000, 0.10% up to £2 million, then free)

- Share-holding annual cap increased: from £45 to £150 per account per year — a more than threefold rise, which affects larger share-heavy portfolios most significantly

- Online share dealing reduced: from £11.95 to £6.95 per trade (£3.95 after 20+ trades in the same month)

- New fund dealing charge introduced: £1.95 per online fund trade (previously free) — though buying funds via regular Direct Debit or dividend reinvestment remains free

- Ready-Made Pension Plan fee reduced: from 0.75% to 0.45% total annual charge

HL estimates that around 8 in 10 clients are better off or pay the same under the new structure. The main beneficiaries are investors with fund-heavy SIPP portfolios under £250,000. The main losers are investors with large share-heavy SIPPs who previously benefited from the £45 annual cap — those investors now pay up to £150 per year just for the share-holding charge.

Understanding these Hargreaves Lansdown SIPP charges helps investors balance cost with service quality. For most fund-based investors below £250,000, the March 2026 changes represent a net saving.

Available Investment Products

Hargreaves Lansdown offers one of the broadest investment selections among UK SIPP providers:

- Thousands of options, including UK and international shares, funds (over 2,500), ETFs, investment trusts, bonds, and a cash management feature

- "Ready-Made Pension Plan" portfolios are available as a passive, lower-cost option with predefined risk levels (e.g., Cautious, Pension Builder, Adventurous, Ethical) — now charged at 0.45% total annual fee, down from 0.75%. New SIPP clients can try it free for up to a year (offer applies until 31 July 2026)

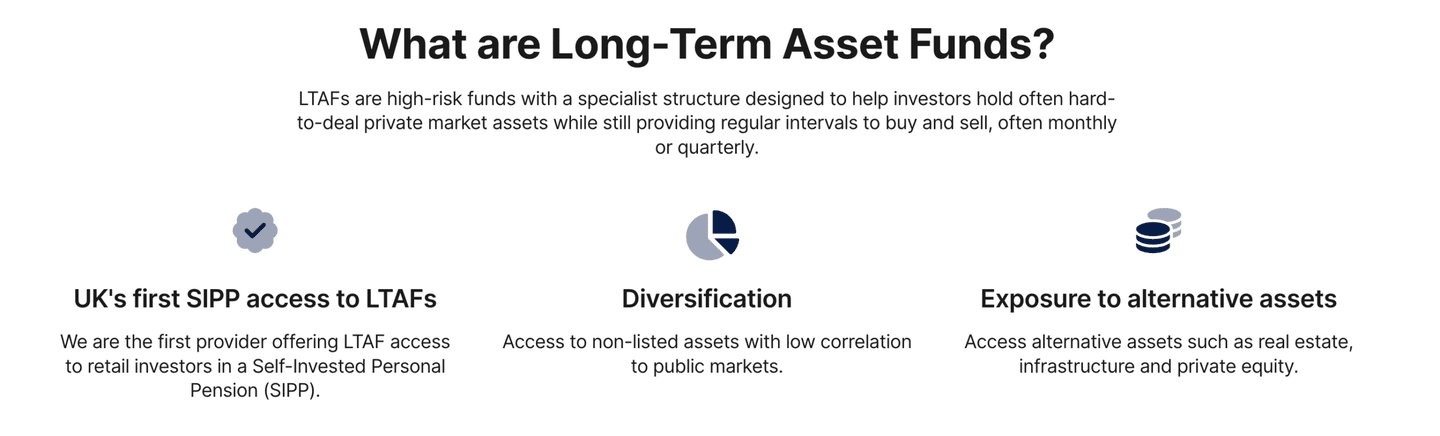

- HL also offers access to Long Term Asset Funds (LTAFs) — private-market, blended funds (e.g., private equity, infrastructure) — though these require a higher minimum investment and have notice periods for withdrawals

Who Is Hargreaves Lansdown's SIPP Best Suited to?

| Novice Investors | For beginners, Hargreaves Lansdown provides extensive educational materials, model portfolios, and investment advice, making the SIPP approachable and easier to understand. The Ready-Made Pension Plan (now 0.45% total, free for up to a year for new clients) is a good entry point. |

| Expert Investors | More experienced investors appreciate the vast investment universe and advanced research tools HL offers, allowing for highly customised portfolios. Note that the new share-holding cap of £150/year applies to share-heavy accounts. |

| Retirees | Retirees benefit from the flexible withdrawal options and the ability to hold a diversified mix of investments within the SIPP to match their income needs. Those making regular fund withdrawals in drawdown should factor in the new £1.95 per fund deal charge. |

Comparing Hargreaves Lansdown's SIPP With Other Providers

Following HL's March 2026 fee overhaul, the competitive landscape has shifted. Here is how HL compares to key alternatives:

| Platform | Annual platform fee | Share cap | Online share dealing | Fund dealing |

|---|---|---|---|---|

| Hargreaves Lansdown | 0.35% (capped £150/yr for shares) | £150/yr | £6.95 (£3.95 after 20+) | £1.95 |

| AJ Bell | 0.25% (capped £3.50/month for shares) | £42/yr | £9.95 | £1.50 |

| Vanguard | 0.15% (capped £375/yr) | N/A (funds only) | N/A | Free |

| Interactive Investor | Flat £12.99–£19.99/month | Included | £3.99 (2 free/month) | Free |

Fees verified from published sources as at March 2026. Always check current rates directly with the provider before making any decisions.

AJ Bell

AJ Bell offers a similar service but with lower share-holding costs — its annual cap is £42 versus HL's £150, making it more attractive for larger share-heavy SIPPs. It also provides a broad investment range and decent research tools, though some investors find HL's platform more intuitive.

👉 For more information, read our AJ Bell review

Barclays

Barclays is a well-established SIPP provider, known for its strong brand and integrated banking services. While it offers a solid investment platform and convenient access for existing Barclays customers, its SIPP offering is less flexible and has a more limited investment range compared to providers like Hargreaves Lansdown.

👉 Read our Barclays smart investor review for more information

Vanguard

Vanguard is a strong SIPP provider for investors looking for a low-cost, simplified approach. It's particularly well-suited for beginners and long-term, passive investors, offering access exclusively to its own high-quality index and ETF funds. The platform fee is 0.15% capped at £375 per year, with free fund dealing. The limited investment range (no individual shares or third-party funds) may not suit those looking for greater flexibility, but it remains the cheapest option for purely fund-based drawdown investors.

👉 If you're interested in Vanguard, read our Vanguard review to learn more

Interactive Investor (ii)

Interactive Investor stands out for its flat-fee pricing model, making it one of the best options for larger portfolios. Investors pay a fixed monthly fee (£12.99–£19.99/month depending on plan) regardless of portfolio size — this becomes increasingly cost-effective as your SIPP grows. ii offers a wide investment range, including shares, funds, investment trusts, and ETFs, along with strong research tools. The crossover point where ii becomes cheaper than HL is roughly around £50,000–£100,000, depending on investment style.

👉 Read here for more on ii: interactive investor review

How to open a SIPP account?

Who Is Eligible?

Anyone aged 18 or over can open a SIPP with HL. Parents or guardians can open SIPPs on behalf of minors, managing the account until the child turns 16. You can contribute up to £60,000 per tax year (the Annual Allowance for 2026/27) and receive tax relief of between 20% and 45% depending on your income tax bracket.

What Is the Process?

Opening a SIPP is straightforward via the HL website. You complete an application, provide identification, and transfer funds either from an existing pension or through new contributions. The platform guides you through investment choices and paperwork efficiently.

Platform

User Interface & Experience

HL's platform is praised for being intuitive and user-friendly, suitable for both desktop and mobile users. Investors can easily track portfolio performance, make trades, and access research reports.

Tools & Resources Available

HL offers a range of tools such as retirement calculators, portfolio health checks, expert market commentary, and a fee comparison calculator (available at hl.co.uk/help/fees/calculator) to help investors understand the impact of the new March 2026 charges.

Mobile App Review

The mobile app mirrors the desktop experience well, allowing on-the-go portfolio management, research access, and trade execution, which many users find convenient. HL has won Best for Customer Service and Best Investment App awards for 2026.

Customer Service

Hargreaves Lansdown offers highly-regarded and exclusive customer support via:

- Phone: 8am till 5pm on business days and 9:30am–12:30pm Saturday.

- Via message on their website

You can also book an in-person meeting with Hargreaves Lansdown's financial advisor at their London office, by telephone, or through one of their Bristol representatives.

FAQs

Is my money safe with HL SIPP?

Hargreaves Lansdown is fully regulated by the Financial Conduct Authority (FCA), ensuring strict oversight and protection for investors. Client assets are held in segregated accounts and protected by the FSCS up to £85,000 per provider in the event of HL insolvency.

What changed with HL SIPP fees in 2026?

On 1 March 2026, HL implemented its first major fee overhaul in over 10 years. The headline platform charge was cut from 0.45% to 0.35%, share dealing was reduced from £11.95 to £6.95, and the Ready-Made Pension Plan fee fell from 0.75% to 0.45%. However, the annual share-holding cap was raised from £45 to £150 per account, and a new £1.95 fund dealing charge was introduced for online fund trades (buying via Direct Debit remains free). HL estimates 8 in 10 clients are better off or pay the same.

Does Hargreaves Lansdown offer alternative accounts?

Yes, beyond SIPPs, HL also offers ISAs, Junior ISAs, Lifetime ISAs, and general investment accounts. This ecosystem allows investors to manage various savings and investment goals in one place, simplifying financial planning.

Can I manage my investments online with a Hargreaves Lansdown SIPP?

Yes, you can manage your SIPP completely online. The platform supports a variety of convenient features like automated monthly investing via Direct Debits from as little as £25, plus easy pension transfers and a seamless user interface.

You have full access to their platform via both web and mobile app, allowing you to monitor your portfolio, make contributions, adjust investments, and trade in real time.